It Gets Complicated

- National Bank of Canada

- Jul 7, 2022

- 7 min read

CIO Office National Bank Investments

National Bank Investments

Market Update │ July 2022

Highlights

After an eventful first half of the year, returns across asset classes remain tinged with red as substantially higher than expected inflation, followed by a forceful response from the Fed, has pushed U.S. equities into bear market territory.

Until recently, base-case economic scenario called for slower (albeit still strong) growth and lower (albeit still high) inflation, a backdrop that would have allowed the Fed to quickly raise its policy rate to neutral but not into restrictive territory. Now, while there are still reasonable chances this scenario will ultimately materialize over the second half of the year, the precariousness of the current economic environment interjects more uncertainty in our outlook with greater downside risks, and the next few months promise to remain very volatile as a result.

Is all the bad news already fully discounted in current market prices? The bar has certainly been lowered for stocks. However, bear market history shows that a sustained equity recovery usually requires a pivot by the Federal Reserve. The challenge: barring a precipitous deterioration in the economic environment, the current inflationary situation implies this shift on the monetary front is likely to be some time away. Meanwhile, the outlook for bonds is increasingly competing with that of equities, with yields often near levels not seen in a decade.

Market Review

Fixed Income

Following slight relief in May, June again saw significant losses for fixed-income securities as the Federal Reserve and the Bank of Canada turned even more hawkish on inflation. This is the sixth consecutive month of losses for the Canadian bond universe, down 11.9% year-to-date.

In the U.S., as recession fears grew, high-yield corporate bonds fell more than the safer investment-grade bonds.

Equities

June was a very difficult month for global equity markets as investor sentiment was undermined by persistent inflation, Fed tightening, and recession fears. The energy sector, which had performed extremely well in the first five months of the year, also suffered heavy losses in June as oil prices fell.

Emerging markets slightly outperformed the rest of the world on a monthly basis, as China announced new stimulus measures and relaxed public health restrictions.

FX & Commodities

Most commodity prices declined in June, including oil, gold, copper, and several agricultural commodities.

With investor sentiment deteriorating significantly during the month, the U.S. dollar resumed the rally that began earlier this year. The Greenback appreciated 2.9% in June and is now 9.1% stronger than at the beginning of the year.

It gets complicated

After an eventful first half of the year, returns across asset classes remain tinged with red, with a few exceptions (Chart 1).

Incidentally, June turned out to be quite volatile for U.S. stocks, as a brief rebound early in the month was succeeded by a swift drop into bear market territory – the first since March 2020 and only the sixth since 1980 (Chart 2).

Triggering this downturn was the announcement of inflation figures well above expectations in the United States. Not only did the annual growth rate of the Consumer Price Index (CPI) accelerated to 8.6% in May (Chart 3) but, more worryingly, the monthly pace of the median CPI calculated by the Cleveland Fed – probably one of the best indicators of underlying inflationary pressures – reached a new record high (Chart 4).

Faced with such data, the Federal Reserve has hardened its stance once again, opting for a 75-bp rate hike – a first since 1994 – and projecting another 175 bps in hikes over the coming six months. On our side of the border, the next Bank of Canada meeting is scheduled for July 13, but inflation here being well above target is also leading markets to expect a 75-bp hike and a 3.5% target rate by year-end (Chart 5).

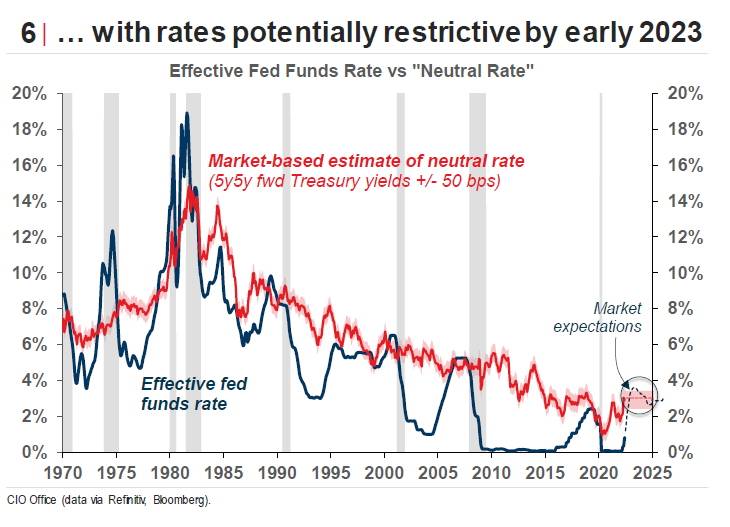

All else equal, this means that U.S. monetary policy is likely to fall into restrictive territory as early as the start of 2023, which, over the past five decades, has always ultimately resulted in a recession (Chart 6).

Reflecting upon these developments, the bond market has started to signal a growing likelihood of recession via an increased number of inversions within the yield curve. While this measure has not yet crossed its more probing threshold, there is little doubt that it will soon do so if the Fed does not lower its rate-hike intentions by the end of the year (Chart 7).

An inevitable growth slowdown…

While a recession is not inevitable, it is clear that economic growth will continue to slow in the coming months and that downside risks are prevalent. Concretely, our colleagues from the Economics and Strategy team are projecting positive albeit below-potential real U.S. growth for the second half of 2022 (1.3% in Q3 and 0.8% in Q4) as well as in 2023 (1.5%).

Key factors behind these lowered expectations are financial conditions, which have already tightened significantly in response to the Fed's rate-hike intentions. Consider mortgage and corporate borrowing rates that are near 10-year highs, the U.S. dollar index (DXY) at its strongest in 20 years, and the stock market (S&P 500) which just experienced its worst first half of a year since 1970. These are all elements that weigh on growth, as reflected in the Goldman Sachs Financial Conditions Index (Chart 8).

In addition, inflation itself is also starting to have an ever-more negative impact on the growth outlook. While excess savings accumulated during the pandemic provide some cushion against the rising cost of living, new monthly real disposable income (adjusted for inflation) is now evolving below its pre-2020 trend. Sooner or later, this will affect consumer spending, which is slow to its pre-pandemic trend (also adjusted for inflation, Chart 9), and examples of this phenomenon are growing.

Corroborating these observations, the University of Michigan's Consumer Sentiment Index – which tends to be driven by the level of inflation and unemployment – recently hit an all-time low (Chart 10).

Needless to say, one cannot blame the unemployment rate for undermining consumer sentiment these days. After all, it is still near an historic low with almost twice as many job openings as there are unemployed, a labour market picture far from consistent with a recessionary environment (Chart 11).

That said, we will have to keep a close eye on the evolution of employment, given that a slowdown in inflation will necessarily require a cooling of the overheated labour market. The big question is whether central banks will manage to find the perfect dose of monetary tightening to accomplish this without tipping the scales too far in the other direction. This is no small task.

… but what about inflation?

To be clear: with all the headwinds that economic growth is currently facing, the scenario of a gradual slowdown in inflation over the coming year remains most likely. In fact, this is still what is expected in the inflation SWAP market, where prospects have even declined compared to last month (Chart 12).

Furthermore, the sharp decline in the price of several commodities – especially in agriculture and industrial metals – in recent days is a step in the right direction (Chart 13).

Nevertheless, in the near term, a series of factors of uncertainty over which central banks have little control are complicating the situation. Among these, the most important is undoubtedly the price of a barrel of oil, largely impacted by ongoing geopolitical tensions with Russia. Indeed, black gold has a major influence on energy prices (Chart 14) which, in turn, tend to dictate the direction of overall inflation (Chart 15).

Under normal circumstances, one would expect any specific month's inflation figures to have little impact on Fed policy intentions, especially when they are influenced by such volatile items as energy. Yet, there is nothing normal about the current state of affairs, as the Fed has committed to continue its aggressive monetary tightening (and even accelerate it) until it sees "convincing evidence" 3 that inflation is falling.

What would constitute such a thing is not entirely clear. However, it can be assumed that a minimum of three months of lower inflation data will be required. In addition, a simple return to monthly figures one standard deviation above the historical average – which would already be a marked improvement compared to the last six months – will probably not be sufficient, as the year-over-year pace would remain above 8% throughout the rest of 2022 (Chart 16).

The Bottom Line

Until recently, our base-case economic scenario called for slower (albeit still strong) growth and lower (albeit still high) inflation, a backdrop that would have allowed the Fed to quickly raise its policy rate to neutral but not into restrictive territory. Now, while there are still reasonable chances this scenario will ultimately materialize over the second half of the year, the precariousness of the current economic environment interjects more uncertainty in our outlook with greater downside risks, and the next few months promise to remain very volatile as a result.

Is all the bad news already fully discounted in current market prices? After all, the sharp rise in real yields has dragged the S&P 500's price/earnings (P/E) ratio down from 22x to 16x year-to-date (Chart 17), a multiple correction in line with what we see on average at the worst of a bear market. In addition, recession fears seem increasingly mainstream, judging by Google Search trends (Chart 18).

The bar has certainly been lowered for stocks. However, the earnings season that’s just around the corner will most likely see profit expectations being revised downward in light of the latest economic developments. In the U.S., earnings expectations remain particularly elevated – around 10% for 2022 and 2023 (Chart 19) –, a factor to take into account when interpreting valuation ratios based on such estimates.

What’s more, bear market history (the subject of our last strategic report available here) shows that a sustained stock market recovery usually requires a pivot by the Federal Reserve (Chart 20). Unless economic conditions deteriorate precipitously, the current inflationary environment implies that this shift on the monetary front is likely to be some time away.

On the flip side, the outlook for bonds is increasingly competing with that of equities, with yields often near levels not seen in 10 years. Although the Fed's latest projections suggest a slight upward potential for 10-year Treasury yields (Chart 21), their current levels imply more attractive risk/reward properties for the asset class on a forward-looking basis (Chart 22). For instance, while a slowdown in inflation would likely lead to a simultaneous rally in bonds and equities, a more adverse economic scenario should ultimately allow the asset class to do well as yield curves would invert.

The Canadian market is trading at particularly attractive valuation levels despite outperforming its peers in 2022 (Chart 23). In the U.S., the S&P 500's greater exposure to growth leaves the Index more sensitive to inflation dynamics, while the risk of earnings downgrades appear greater in the near term.

For emerging markets, the situation remains precarious. However, China, which was already in monetary-tightening mode last year, is now adopting increasingly accommodative policies that could allow the world's second-largest economy to recover from its lows in the second half of the year, provided the COVID-19 cases remain under control. This potential divergence from the rest of the world would not be unprecedented (Chart 24) and will certainly be a trend to monitor closely for the remainder of the year.

Comments